It is easy to focus only on the negative so it is helpful to seek out the opportunities for banks to contribute positively to addressing climate issues. Two New Yorker articles over the last few months provide examples of business ideas that should be sources of good bank lending opportunities. Both are in the area of food production – thereby also meeting a core human need of sustenance. In September 2019 the New Yorker had extensive coverage of the emerging meat substitute industry. In its most recent edition, the New Yorker covered an alternative approach to farming that seeks to work with nature whilst delivering sustainable and substantial returns. These are both areas where bank financing will be need to encourage the transition to food production that meets the needs of a large population whilst maintaining the environment. Food related bankers should be focusing on these opportunities.

The carbon stress test – is your portfolio ready?

In an excellent and detailed article, Lex in the Financial Times highlights the substantial financial risk of stranded assets in carbon based fuels, estimated at over USD 900 billion. Although the focus of the article is more from an equity investment perspective, it provides a very useful context for banks to look at their exposures as well. Mark Carney, Governor of the Bank of England, has been noting this point for some time and has been encouraging banks to look at the risks on their balance sheets. His thoughts are usefully summarised in a Guardian article at the end of last year. Is your bank looking at this risk in its portfolio?

Let the sunshine in . . .

For bankers transparency is often a challenge. Confidentiality when used to protect the information of a client is worthwhile. However, banks too often use confidentiality to avoid public knowledge for challenges they face or errors they make. Recently HSBC settled an employment issue with the result that a potential whistleblower would not publicly provide information that might have been embarrassing. Credit Suisse similarly has not been public about their efforts to get information on Greenpeace regarding their focus on reducing Credit Suisse’s involvement in financing carbon related projects. In both cases the information slowly will come to the surface and likely lead to reputational damage. But then the real question should be why no one in the bank management challenged the dubious activities in the first place!!!

Treating clients as people – not profit centers

Nicholas Kristof in the New York Times covers a story that reflects poorly not only on the bank named but also on the banking industry. The story focuses on the application of policies, often installed for good reasons, but with no flexibility for treating a client as a person. Whilst one can be outraged by the results of the personnel policies highlighted in this story that led to the dismissal of a call center employee and her supervisor, there is also the underlying reason for the client problem. In the very first paragraph it notes that the client “had deposited a $1,080 paycheck into his account at U.S. Bank. The bank put a hold on most of the sum.” At a time of increasing technology, is it still necessary to hold funds for long periods of time and prevent clients from accessing their money? Or is this just a way for the bank to profit from a client’s money?

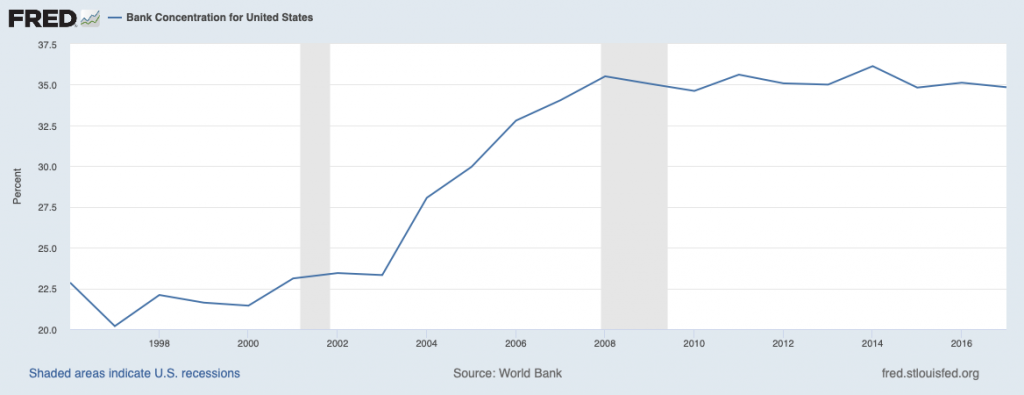

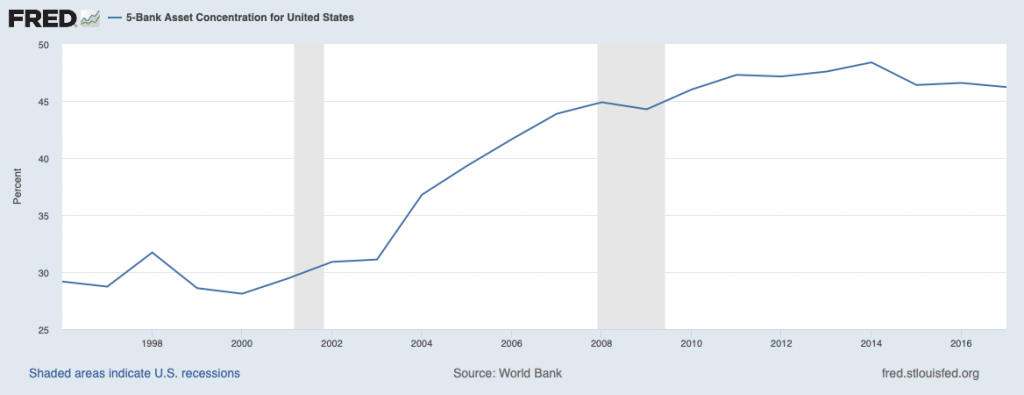

Overly concentrated banking – does diversity matter?

In Tuesday’s Financial Times, Robert Armstrong noted that the discussion on too big to fail in the US needed a new framework for discussion. He states that the impact of economies of scale in the US banking industry have led to higher concentrations. He is rather sanguine on the consequences of this development and notes that it is likely to continue. The concentration in the US can be seen in the following charts (alas data only available through yearend 2017):

A fundamental question to address is the impact of higher concentration. A standard concern is the increased vulnerability of the banking system as it becomes more concentrated – the too big to fail argument. However, it is possible that larger banks lose their capability to meet the needs of local clients – individuals and enterprises – as decision making becomes more centralised and removed from communities. Local community-based banks have historically provided finance for the new entrepreneur whose needs and situation benefit from local knowledge.

This concentration accelerated substantially after 2002. I believe it was driven by two factors: investment requirements for technology and additional regulatory complexity. Both factors create substantial fixed costs that are more easily absorbed by larger banks. Addressing these underlying causes of reduced diversity is essential to preserving a robust banking system that can meet the needs of local communities.

“The mills of justice grind too late as to make wickedness fearless”

Many centuries ago Plutarch noted: “Thus, I do not see what use there is in those mills of the gods said to grind so late as to render punishment hard to be recognized, and to make wickedness fearless.” This lesson continues today as justice for misbehaviour in banking occurs slowly as highlighted in articles published today.

In the New York Times there was an extensive article on the use of financial engineering to effectively “steal” taxes from primarily European governments. These transactions were supported by many major banks, consultancies, legal firms and accounting firms and led to an estimated loss of $60 billion in tax revenues. Of course some of those funds went to the profits of the banks but also were undoubtedly use to pay substantial bonuses and fees to all involved. These activities are further covered in the Financial Times with yet another bank being in the spotlight of prosecutors.Paragraph

Meanwhile in the US there was a substantial fine assessed against senior bank managers for their role in fostering “a toxic sales culture that foisted unwanted products and sham bank accounts on millions of customers.” This article in the New York Times noted that further fines and other enforcement actions are likely against additional senior managers at the same bank.

The common thread through these stories is an internal culture on focused on making profits with no apparent regard as to whether the activities served any positive society purpose. Is it any wonder that bankers have poor reputations?

Looking for risk in all the right places

A recent publication from McKinsey provides a useful road map for bankers focused on risk from climate change. This publication not only provides a solid overview of the scientific facts supporting the view that climate change is real but goes further to highlight the many risks arising from climate change that can impact the risks of loans and investments made by banks. The questions remains which banks are focusing on identifying and mitigating these risks? And which regulators are incorporating these risks in their stress tests?#ban

Investors are coming for you – is your bank ready???

The pressure on banks to be responsible in their lending relative to climate impact is growing. ShareAction has led a group of investors in filing the first climate related shareholder resolution in Europe. This resolution to be taken up at the Barclays annual meeting is likely to be only the beginning of pressure from investors for banks to be proactive in ensuring that their lending and related financing activities are supportive of the Paris goals. This action is consistent with the comments from Huw Steenis in today’s Financial Times that further highlights the future demands on banks. But how many banks are prepared to respond to this pressure? Or do most banks hope this issue will just go away?

#bankingonvalues

Heads I win, tails you lose

A recent paper from Goodhart and Lastra focuses on the danger posed by limited liability for bank management. They “advocate moving towards a two-tier equity system, primarily for banks, with insiders, senior managers and others with influence over corporate decisions, becoming subject to multiple liability” to address these dangers. As noted by Jonathan Ford in the Financial Times, “by making insiders financially accountable for their actions, it would rebalance the calculus of fear versus greed.” Clearly the lack of accountability for the financial crisis for nearly all bank managers is an issue that needs to be addressed. But are the banks ready to make this change or do they prefer (as managers) to be immune from the consequences of their actions.

Remembering Sir Fazle Abed

As we enter a new decade I would like to remember Sir Fazle Abed who I had the good fortune to meet and learn from whilst at the Global Alliance for Banking on Values. His holistic commitment to addressing the challenges facing society – economic, social and environmental – was a great lesson for me. He provides a role model for many but especially for bankers seeking to move their business models to a focus on addressing the needs of society.

His story was captured well by the New York Times in an obituary published 1 January. His impact and values were captured even better by my colleague and friend, Laurie Spengler, who worked directly with him for many years in a LinkedIn post. And the impact he made on a personal level can be seen in this video.